Record revealed

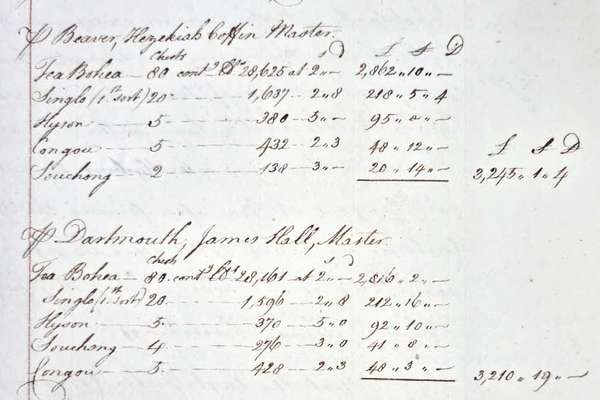

Request for compensation for the Boston Tea Party

On 16 December 1773, 340 chests of tea were thrown into Boston harbour by protesting colonists. This letter from the East India Company requests reimbursement.

Series

Catalogue reference: IR 88

IR 88

These records of the Chief Inspector of Taxes give details of the assessments for income tax on persons, corporations, companies or societies.

These records of the Chief Inspector of Taxes give details of the assessments for income tax on persons, corporations, companies or societies.

The books are arranged in alphabetical order of Tax Office for each year selected.

Tax Offices record in Schedule D Assessment books the full name and address of individuals, partnerships or companies assessed, a description of the trade, profession or vocation, the amount of the profits or income assessed and the tax charged.

Income tax chargeable under Schedule D is divided into the following six 'Cases':

Case I Profits (not included in any other schedule) arising from any trade, manufacture, adventure or concern in the nature of trade.

Case II Profits (not included in any other schedule) arising from any profession or vocation.

Case III Interest, discounts and other annual payments received in full without deduction of tax.

Case IV Interest (not included in any other schedule) arising from securities outside of the United Kingdom.

Case V Income arising from possessions outside of the United Kingdom.

Case VI Any annual profits or gain not falling under any other case of Schedule D or included in any other schedule.

Board of Inland Revenue: Chief Inspector of Taxes' Branch and successors: Schedule D Assessment Books

Read stories that share a catalogue subject with this record.

Record revealed

Focus on

Record revealed

Records that share similar topics with this record.