Record revealed

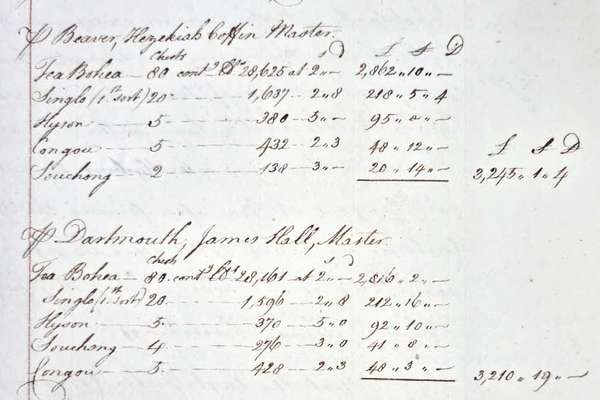

Request for compensation for the Boston Tea Party

On 16 December 1773, 340 chests of tea were thrown into Boston harbour by protesting colonists. This letter from the East India Company requests reimbursement.

Department

Catalogue reference: CV

CV

Records of the Value Added Tax Tribunals settling disputes arising from the administration of value added tax (VAT) and assisting in obtaining uniformity in the application of the tax throughout the United Kingdom.Decisions of the Tribunals are...

Records of the Value Added Tax Tribunals settling disputes arising from the administration of value added tax (VAT) and assisting in obtaining uniformity in the application of the tax throughout the United Kingdom.

Decisions of the Tribunals are in CV 6, with indexes in CV 5. Printed reports of appeals to the Tribunals, selected by the president for publication, are in CV 1 and related case files are in CV 2. Instructions concerning the administration of appeals are in CV 3 and practice notes and directions, issued by the president for the guidance of chairmen, are in CV 4. Administration files are in CV 7

Records of the Combined Tax Tribunal are in: LB

From 1980 Value Added Tax Tribunals

By the Finance Act 1972 (and later the Value Added Tax Act 1983), Value Added Tax Tribunals for England, Wales, Scotland and Northern Ireland were established under a president appointed by the Lord Chancellor. The tribunals were appointed to deal speedily and with a minimum of formality with appeals against decisions of the Commissioners of Customs and Excise concerning value added tax, particularly as regards registration for the purposes of the tax and concerning the amount of tax chargeable or deductible, and to assist in obtaining uniformity in the application of the tax throughout the United Kingdom.

The tribunals are entirely independent of the Commissioners, being under the supervision of the Council on Tribunals. They consist of the president or, if so authorised by the president, a member from the appropriate panel of chairmen, sitting with two other members, or with one other member or alone. There are three panels of chairmen and three panels of other members for England and Wales, Scotland, and Northern Ireland respectively. Members of the panel of chairmen in England and Wales are appointed by the Lord Chancellor. In Scotland they are appointed by the Lord President of the Court of Sessions, and in Northern Ireland by the Lord Chief Justice of Northern Ireland. Appointments to panels of other members are made by the Treasury.

In England and Wales, Value Added Tax Tribunals are established in London, Cardiff, Birmingham and Manchester. In Scotland and Northern Ireland they are established in Edinburgh and Belfast respectively.

Following the Finance Act 1985, the Value Added Tax Tribunals transferred to the Lord Chancellor's Department on 1 April 1986. Between October 1994 and January 1995 the Value Added Tax Tribunals took on four new jurisdictions: appeals tribunal for air passenger duty; insurance premium tax; excise duties; and customs duties, and was subsequently renamed the VAT and Duties Tribunals.

ln England and Wales, a party dissatisfied in point of law by a decision of a Value Added Tax Tribunal may appeal to the High Court of Justice. In Scotland a similar appeal lies to the Court of Sessions, and in Northern Ireland to the High Court of Justice in Northern Ireland.

Records of Value Added Tax Tribunals

Read stories that share a catalogue subject with this record.

Record revealed

Focus on

Record revealed

Records that share similar topics with this record.