Record revealed

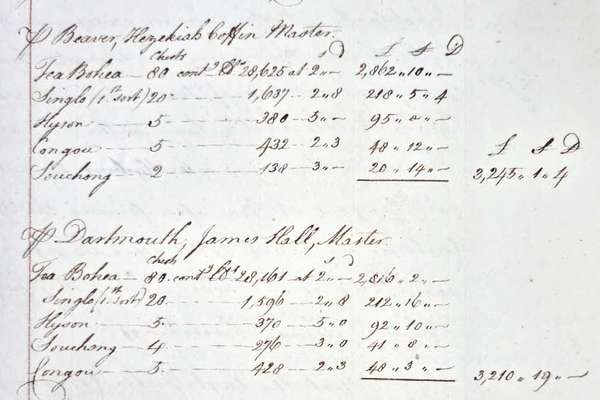

Request for compensation for the Boston Tea Party

On 16 December 1773, 340 chests of tea were thrown into Boston harbour by protesting colonists. This letter from the East India Company requests reimbursement.

Series

Catalogue reference: CV 7

CV 7

This Series contains files relating to the establishment, organisation and staffing of Value Added Tax Tribunals; the review, revision and reprint of their forms; copies of their decisions and proposals for their merger with the Special...

This Series contains files relating to the establishment, organisation and staffing of Value Added Tax Tribunals; the review, revision and reprint of their forms; copies of their decisions and proposals for their merger with the Special Commissioners of Income Tax.

Records of the Special Commissioners of Income Tax are in EM 1-EM 4. EM 1 EM 2 EM 3 EM 4

The Court Service in 2001

Combined Tax Tribunal in 2001

Value added tax was introduced by the Finance Act 1972 and section 40 of the Act, in accordance with Schedule 6, constituted value added tax tribunals for the purpose of appeals against decisions of the Commissioners.

Value added tax tribunals were established for England and Wales, Scotland and Northern Ireland respectively. The Schedule provided for a President, to be appointed by the Lord Chancellor. The President, with the consent of the Treasury, determined the number of tribunals and when and where they should sit. Each tribunal was to consist of a chairman sitting, either with two other members, or with one other member, or alone.

The Commissioners were empowered to make rules with respect to the procedure to be followed on appeals to value added tax tribunals and such rules included provisions: for limiting the time within which appeals could be brought; for enabling hearings to be held in private; for parties to be represented; for requiring persons to attend to give evidence and produce documents; for the payment of expenses to persons attending as witnesses; for the award and recovery of costs; and for authorising the administration of oaths to witnesses.

The constitution and procedure of value added tax tribunals were further ratified by Section 40, Schedule 8 of the Value Added Tax Act 1983 and Section 30, Schedule 8 of the Finance Act 1985 .

The files created by the Value Added Tax Tribunals and the Special Commissioners of Income Tax were transferred, upon amalgamation, to the Combined Tax Tribunals in 1992.

Value Added Tax Tribunals: Administration Files

Read stories that share a catalogue subject with this record.

Record revealed

Focus on

Record revealed

Records that share similar topics with this record.