Record revealed

Jane Austen’s will

Explore Jane Austen's will, in her own handwriting, which shows how the novelist planned to share her belongings with family and friends after her death.

Division

Catalogue reference: Division within IR

Division within IR

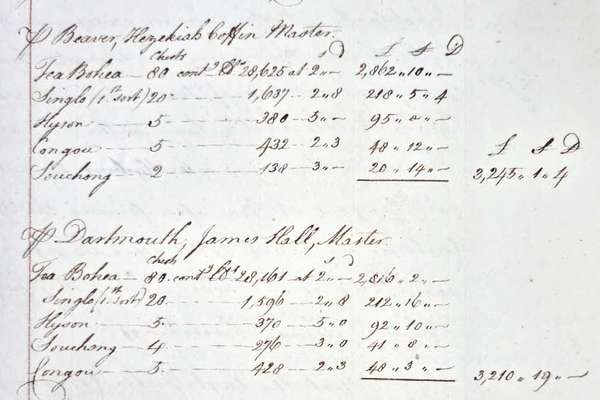

Records reflecting the creating bodies' responsibilities in relation to the administration, assessment and collection of death duties, capital transfer tax, and inheritance tax. Death duty registers are in IR 26, with indexes in IR 27. Board...

Records reflecting the creating bodies' responsibilities in relation to the administration, assessment and collection of death duties, capital transfer tax, and inheritance tax.

Death duty registers are in IR 26, with indexes in IR 27. Board papers dealing with the administration of the duties are in IR 62 and case books in IR 67. Specimens of death duty accounts are in IR 19, with selected death duty accounts of many persons well-known in national life are in IR 59. Letters concerning contentious cases are in IR 6, with Scottish papers in IR 7. Reports to the Treasury on legacy duty cases are in IR 50. Copies of Wills, formerly in IR 5, were disposed of under the Public Records Act 1958 s6.

Petitions against assessments for estate or succession duty are in E 188

A volume, originating in the Board of Stamps, containing comptroller's reports to the Board, is in

In 1796, legacy duty was imposed and regulated by the Legacy Duty Act 1796. Legacy duty was a tax payable on legacies and residues of personal estate of deceased persons. Such duties were only payable on certain types of bequests and only by certain persons defined by their degree of consanguinity (blood-relationship) to the deceased. Through further Acts such as the Legacy Duty Act 1805 and the Stamp Act 1815, this duty was extended to cash legacies and residues bequeathed in wills which were to be raised by the sale of real estate, but not to the acquisition of real estate as such. By the same Acts, the group of beneficiaries liable to pay the duty was also enlarged.

Legacy duty was administered by the Board of Stamps, and a strengthened and reconstituted Legacy Duty Office was set up in 1812 under that Board. In 1834 the Board of Stamps was succeeded by the Board of Stamps and Taxes, which in 1849 was succeeded by the Board of Inland Revenue.

In 1853, succession duty was first imposed by Gladstone under the Succession Duty Act 1853. This was payable on the gratuitous acquisition of property on death, whether this was the personal estate, real estate or leasehold of the deceased. Succession duty was added to the Legacy Duty Office's responsibilities, and the Office was renamed the Legacy and Succession Duty Office.

In 1894, estate duty was imposed by Part 1 of the Finance Act 1894. It superseded probate duty and account duty and was chargeable on all property passing on death, without regard to the relationship of the beneficiaries to the deceased owner.

In 1899, the Legacy and Succession Duty Office was renamed the Estate Duty Office.

In 1949, legacy and succession duties were repealed under Part III of the Finance Act 1949, and the only death duty then in force was the estate duty. The Estate Duty Office, headed from 1919 by a controller of death duties, handled the assessment and collection of this duty. For its assessment work, the Office had access to all wills and administrations and had authority to call for all settlements, deeds of gift and other documents under which claims for death duty might arise. An abstract of all such claims was made in registers compiled for the purpose. There was a separate Scottish office in Edinburgh under a registrar of death duties.

Under the Finance Act 1975 estate duty was abolished and replaced by a capital transfer tax. In January 1977 the Office was renamed the Capital Taxes Office.

Legacy Duty: Succession Duty and Estate Duty records

Read stories that share a catalogue subject with this record.

Record revealed

The story of

Record revealed

Records that share similar topics with this record.