Record revealed

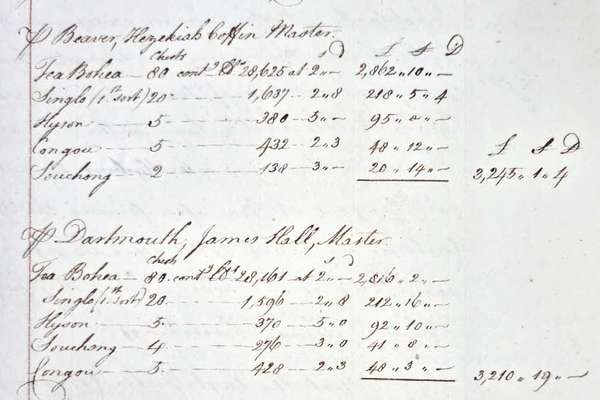

Request for compensation for the Boston Tea Party

On 16 December 1773, 340 chests of tea were thrown into Boston harbour by protesting colonists. This letter from the East India Company requests reimbursement.

Division

Catalogue reference: Division within IR

Division within IR

Records reflecting the responsibilities of the creating bodies in relation to the administration, assessment and collection of income tax, surtax, and other related assessed taxes. Registered files of the Chief Inspector of Taxes' Office are in...

Records reflecting the responsibilities of the creating bodies in relation to the administration, assessment and collection of income tax, surtax, and other related assessed taxes.

Registered files of the Chief Inspector of Taxes' Office are in IR 82, IR 138 and IR 139. Abstracts and statements of tax compiled from returns made by surveyors are in IR 16, with surveyors' property letter books in IR 52 and other property letter books in IR 53. Precedent case books are in IR 54, IR 66 and IR 68. Assessed taxes cases are in IR 12. Corporation duty files are in IR 41. Judges' opinions relating to assessed taxes and inhabited house duties are in IR 70. Schedule D Assessment Books are in IR 88. Examination papers set for candidates for the assistant inspector of taxes grade are in IR 57. Holborn District land tax records are in IR 120, with records of the Committee on Taxation of Land Values in IR 149. Annual reports to the Chief Inspector of Taxes from specialist divisions under his control are in IR 145. Files originally designated for IR 123 have been reassigned.

Miscellaneous books of the Special Commissioners are in IR 86, with instructions concerning their work in IR 112

See also the Records of Special Commissioners of Income Tax in EM

Reports and papers arising from the work of the Royal Commission on Income Tax and other commissions and committees on taxation matters are included in IR 75

Inspectors' ledgers are in

Chief Inspector of Taxes' Office

The administration of income tax has always been locally based (with the exception of the work of the Special Commissioners). Originally authority was placed in the hands of local unpaid bodies of General Commissioners of Income Tax who made assessments, heard appeals, appointed collectors and controlled their accounts. The function of the central government representatives, at first known as surveyors and from 1919 as inspectors, was to protect its interests by ensuring that adequate assessments were made and the duty collected. Over time the executive functions connected with assessment passed to the Board, though assessments were made locally by the General Commissioners until by the Income Tax Management Act 1964 the inspector was made the assessing authority for all income tax and profits tax assessments. The General Commissioner's appellate functions remain and they now form the local appeal tribunal. The determination of the Commissioners on a question of fact is final, but either the taxpayer or the inspector can require them, on a question of law, to state a case for the opinion of the High Court.

The headquarters of the tax surveying staff was originally an Inspector General's Department. In 1860 this was replaced by separate offices under a Chief Inspector and a Chief Examiner, the latter being concerned with arrears of taxes. These departments were amalgamated in 1865. This combined Chief Inspector's Department was in turn united in April 1871 with the Surveying General Examiners' Department which had performed similar functions in regard to the Excise Surveying Establishment. A single inspecting department for both excise and stamps and taxes lasted only until 1876 when separate offices under a Chief Inspector of Taxes and a Chief Inspector of Excise were established, with the latter transferred to the Board of Customs and Excise in 1909.

The primary function of the Chief Inspector of Taxes' Office or Branch was to oversee the assessment of income, profits, corporation and capital gains taxes. It also dealt with claims in respect of tax overpayment and the repayment of post-war credits, and controlled the activities the local tax offices or 'districts' where the bulk of the work was done. There were four principal elements in its organization:

A network of local tax offices (over 700 by 1965), dealing with the day to day work of tax assessment and repayment for their area or 'district'. Each was under the charge of a district inspector who is responsible for the efficient management of the office and a critical examination of accounts.A body of inspecting officers (known as principal inspectors or senior principal inspectors), responsible for monitoring the work of the district inspectors and their offices. In 1965 each inspecting officer dealt with about 14 local tax offices, providing a link between them and the Branch's Head Office in London. About half of the inspecting officers were based in London.The Branch's Head Office at Somerset House, London. In 1965, this comprised the Chief Inspector of Taxes, two deputies (one dealing with establishment and organisation issues, the other with technical issues), 25 senior principal inspectors, and supporting staff. The senior principal inspectors might be called upon to act as inspecting officers, but were principally concerned with gathering information and providing advice on specialised topics. Head Office also included a staffing investigation section (which investigated the staffing requirements of local tax offices); an organisation section (responsible for developing standard procedures, instructions and forms); and a unit dealing with employers' proposals for the establishment or amendment of superannuation funds and pension schemes. In December 1964 the latter was detached from the Chief Inspector of Tax Branch and became an independent branch known as the Superannuation Funds Office under a controller, to deal with employers' proposals for establishing or amending superannuation funds and pensions schemes, which required the Board's approval if they were to be recognised for tax purposes.Specialised offices, including the Public Departments Office at Cardiff and Edinburgh (responsible for the tax affairs of Crown servants and pensioners); the Cardiff Marine District (which dealt with the tax assessment of merchant seamen); the Office of the Chief Inspector (Claims) at Bootle, Lancs (which dealt with all aspects of claims for tax repayment); and the Enquiry Branch, based in London and seven other cities (which investigated major cases of underassessment of taxes).

In 1975 the position of Chief Inspector of Taxes and the Chief Inspector of Taxes Branch were formally abolished. Most of the Branch's functions, including the supervision of local tax offices, were transferred to Inland Revenue's newly created Policy Division and Management Divisions.

Office of Special Commissioners of Income Tax, and the Surtax Office

Commissioners of Income Tax were appointed by the Treasury under the Income Tax Acts 1805 and 1842. Initially their duties included the grant of tax relief to charities on their property income and to foreigners holding public stock. They also carried out assessment work on certain income from annuities and dividends. Income tax was abolished in 1816 but when it was re-imposed in 1842 provision was made for the appointment of a new body of special commissioners with increased powers. To enable taxpayers, particularly small businessmen, to avoid disclosing their affairs to the local and unpaid general commissioners, they could elect to be assessed by these centrally-appointed, expert, and salaried special commissioners. If dissatisfied with an assessment by the Special or General Commissioners a taxpayer could apply to the Special Commissioners to be heard in person by way of an appeal. Other duties of the Special Commissioners included the assessment for tax of foreign and colonial dividends and, from 1860, the profits and gains of railway companies. Through a Claims Branch they also dealt with tax repayment matters although this work passed to the Chief Inspector of Taxes Office in 1920. Their Office, under the direction of the Board as ex-officio Special Commissioners, was included on the establishment of the Secretaries' Office.

In 1909 the Special Commissioners were made responsible for the newly introduced super-tax, re-named surtax in 1927. The Income Tax Management Act 1964 relieved them of this and other executive work, leaving them only with appellate duties as a full-time independent appeal body outside the departmental administration of the Board of Inland Revenue. In most cases appeals against tax assessments take place locally before General Commissioners but taxpayers have an alternative right of appeal to the Special Commissioners. These are heard in London or on circuit and either the taxpayer or the Crown may appeal to the High Court on a point of law against a determination of the Special Commissioners. The Special Commissioners of Income Tax were appointed by the Treasury but supported administratively by the Board of Inland Revenue, until the Finance Act 1984 transferred both functions to the Lord Chancellor's Department.

Following the Income Tax Management Act 1964, the Surtax Office of the Board of Inland Revenue was formed, with the Controller of Surtax as its head. This official was also Inspector of Foreign Dividends and had a small staff to deal with income tax on overseas dividends and interest paid through banks and other agents in this country. Under the Finance Act 1972 surtax was abolished and replaced by a graduated tax on higher incomes.

Records of Income Tax, Land Tax, Property Tax and related assessed taxes

Read stories that share a catalogue subject with this record.

Record revealed

Focus on

Record revealed

Records that share similar topics with this record.